Over the Rainbow: Treasury Allows Gay, Married Couples to File Taxes Jointly

As of September 16, 2013, same-sex, legally married couples must file federal tax returns as married couples – whether they are filing jointly or separately. Both the Internal Revenue Service and the Department of the Treasury announced August 29th that they will now recognize the State of Celebration rather than the State of Residence/Domicile, for federal tax purposes.

The announcement came following the U.S. Supreme Court’s rulings regarding DOMA (Defense of Marriage Act) in June. But what exactly, does the State of Celebration policy mean?

Gay couples married in California but who live in Nevada for example – where same-sex marriage is not recognized – should complete federal tax returns as married, since California sanctions these weddings.

Things get a little more complicated for same-sex couples filing state income taxes where gay marriage is not recognized, i.e. in Hawaii. They may need to file two separate, state returns. Californians won’t need to worry about this though, since our state culls info from the federal filing to apply its own rates to the California income tax return.

This State of Celebration approach by the Treasury and IRS affects the following provisions on federal tax returns:

- Child Tax Credits

- Earned Income

- Employee Benefits

- Gift and Estate Taxes

- IRA Contributions

- Marriage Penalties

Couples who are registered domestic partners or who have same-sex unions will neither benefit, or be affected by, the State of Celebration policy.

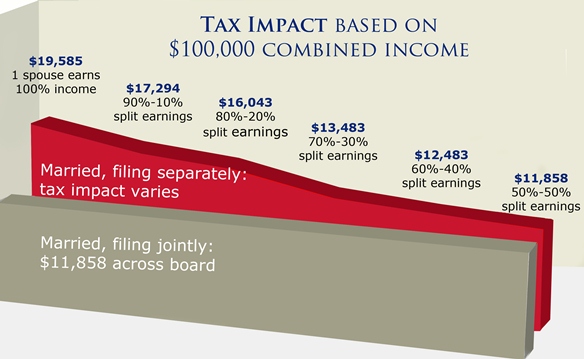

The same-sex couples who will benefit most from the federal policy, are those that have a large disparity in income between the two partners. Tax savings are greatest for those couples with one working spouse, for example.

Based on household income $100K, standard deduction, no children and no tax credits. Source: Bankrate.com.